Aplikasi Trending 2024 Informasi dan Review Aplikasi Terbaru Trending 2024

Aplikasi Trending 2024 Informasi dan Review Aplikasi Terbaru Trending 2024

Introduction

Are you struggling to understand the terms and conditions of your auto insurance policy? Are you confused about what’s covered and what’s not? If yes, then you’re not alone. Many people find it challenging to read and understand their auto insurance policies. But don’t worry, we’re here to help you. In this comprehensive guide, we’ll explain everything you need to know about how to read auto insurance policy.

What is an Auto Insurance Policy?

Before we dive into the details, let’s first understand what an auto insurance policy is. In simple terms, an auto insurance policy is a contract between you and your insurance company that protects you against financial loss if you have an accident or your car is stolen. The policy outlines the terms and conditions of the insurance coverage, including what’s covered, what’s not, and how much you’ll pay for the coverage.

Auto insurance policies can be confusing to read, and the terminology used can be difficult to understand. But it’s essential to know what’s in your policy and what you’re paying for. Understanding your auto insurance policy can help you make informed decisions about your coverage and ensure that you’re adequately protected if something unexpected happens.

How to Read Auto Insurance Policy: Step-by-Step Guide

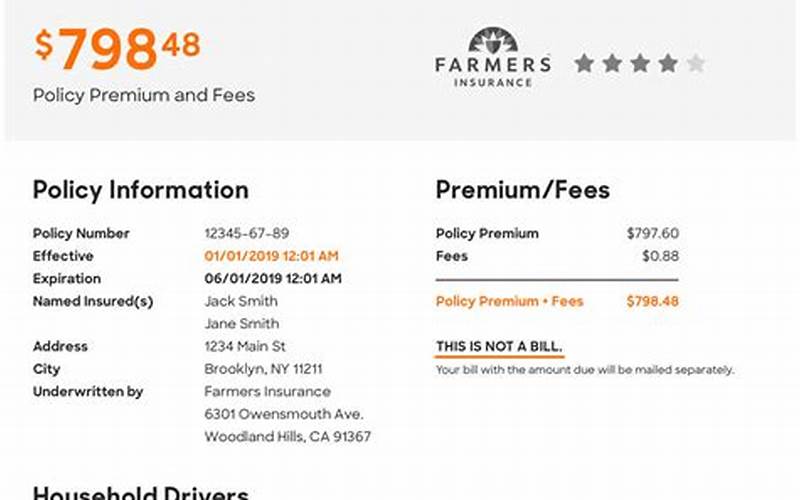

Step 1: Start with the Declarations Page

The declarations page is the first page of your auto insurance policy, and it contains essential information about your coverage. This page typically includes the following information:

- Your name and address

- The make and model of your vehicle

- The policy number

- The coverage limits for liability, collision, and comprehensive

- The deductible for each type of coverage

- The premium for the policy

Make sure to review this page carefully and verify that all the information is correct. If you find any errors, contact your insurance company to get them corrected.

Step 2: Review the Coverage Section

The coverage section of your auto insurance policy outlines the types of coverage you have and how much you’re insured for. This section is divided into three main parts:

- Liability coverage: This covers the costs of damage or injury you cause to someone else or their property while driving your vehicle.

- Collision coverage: This covers the costs of damage to your own car if it’s involved in an accident.

- Comprehensive coverage: This covers the costs of damage to your car that’s caused by something other than an accident, such as theft, vandalism, or natural disasters.

Make sure you understand what’s covered and what’s not covered under each type of coverage. Also, pay close attention to the coverage limits and deductibles for each type of coverage.

Step 3: Check for Exclusions and Limitations

Exclusions and limitations are circumstances under which the insurance company won’t provide coverage. It’s essential to know what these are so that you can avoid them or take steps to get additional coverage if needed. Some common exclusions and limitations include:

- Driving under the influence of drugs or alcohol

- Intentional damage to your own vehicle

- Using your vehicle for commercial purposes

- Participating in racing or other high-speed activities

- Driving in an area where you’re not covered

Make sure to read this section carefully and understand any exclusions or limitations that apply to your policy.

Step 4: Understand the Endorsements

Endorsements are additional coverages that you can add to your policy for an extra cost. These endorsements can provide additional protection, but they can also add to the cost of your insurance. Some common endorsements include:

- Roadside assistance

- Rental car reimbursement

- Accident forgiveness

- Glass coverage

Make sure to review the endorsements offered by your insurance company and consider whether they’re worth the extra cost.

Step 5: Read the Conditions and Responsibilities

The conditions and responsibilities section of your auto insurance policy outlines your obligations as the policyholder and the insurance company’s obligations as the insurer. This section typically includes information about:

- How to file a claim

- What to do after an accident

- When and how to pay your premiums

- How your coverage can be cancelled or renewed

Make sure to read this section carefully and understand your responsibilities as the policyholder. If you have any questions, contact your insurance company for clarification.

Understanding the Terminology

As we mentioned earlier, auto insurance policies can be challenging to read because of the terminology used. Here are some common terms you’ll come across:

Liability

Liability refers to the legal responsibility for something, usually an accident. In the context of auto insurance, liability coverage pays for any damages or injuries you cause to someone else or their property while driving your vehicle.

Deductible

A deductible is the amount of money you’ll have to pay out of pocket before your insurance coverage kicks in. For example, if your deductible is $500, and you have a $2,000 claim, you’ll have to pay $500, and your insurance company will pay the remaining $1,500.

Premium

Your premium is the amount of money you pay for your insurance coverage. This is usually paid on a monthly or yearly basis.

Underwriting

Underwriting is the process that insurance companies use to determine your risk as a customer and set your premiums accordingly. They’ll look at factors such as your age, driving record, and the type of car you drive to determine your risk level.

Claim

A claim is a request for reimbursement from your insurance company. If you have an accident or your car is stolen, you’ll need to file a claim to get reimbursed for the damages.

Exclusion

An exclusion is a circumstance under which your insurance policy won’t provide coverage. For example, if your policy excludes coverage for driving under the influence of drugs or alcohol, and you have an accident while under the influence, your insurance won’t cover the damages.

Limitation

A limitation is a cap on the amount of coverage provided for a particular circumstance. For example, if your liability coverage has a $50,000 limit, and you cause $100,000 in damages, your insurance will only pay up to $50,000, and you’ll be responsible for the remaining $50,000.

FAQs

1. How do I know what’s covered under my auto insurance policy?

You can find out what’s covered under your auto insurance policy by reviewing your declarations page and coverage section. These documents will outline the types of coverage you have and how much you’re insured for. If you’re still unsure, contact your insurance company for clarification.

2. Can I change my coverage limits or deductible?

Yes, you can usually change your coverage limits or deductibles by contacting your insurance company. Keep in mind that changing your coverage may affect your premiums, so make sure to get a quote before making any changes.

3. What should I do if I have an accident?

If you have an accident, you should first make sure that everyone involved is safe and call 911 if necessary. Then, exchange insurance and contact information with the other driver(s) and take pictures of the damage. Finally, contact your insurance company to file a claim.

4. What happens if I don’t pay my insurance premiums on time?

If you don’t pay your insurance premiums on time, your coverage may be cancelled, and you may be charged late fees. Your insurance company may also report your non-payment to credit reporting agencies, which could affect your credit score.

5. Can I cancel my auto insurance policy?

Yes, you can cancel your auto insurance policy at any time. Keep in mind that cancelling your policy may result in a penalty, and you may also lose any discounts you received for being a long-term customer.

6. What happens if I’m in an accident with an uninsured driver?

If you’re in an accident with an uninsured driver, you may be responsible for paying for the damages out of pocket. However, if you have uninsured motorist coverage, your insurance company may be able to help cover the costs.

7. How much does auto insurance cost?

The cost of auto insurance depends on several factors, including your age, driving record, the type of car you drive, and the coverage limits you choose. On average, Americans pay around $1,500 per year for auto insurance, but your premiums may be higher or lower depending on your circumstances.

Conclusion

Reading and understanding your auto insurance policy may seem daunting, but it’s crucial for protecting yourself and your assets. By following the steps outlined in this guide and understanding the terminology used in your policy, you can make informed decisions about your coverage and ensure that you’re adequately protected in case of an accident. If you have any questions or concerns about your policy, don’t hesitate to contact your insurance company for support.

Remember that being an informed consumer is the key to getting the best coverage and rates. So, take the time to review your policy carefully, and make sure you understand what’s covered and what’s not.

If you found this guide helpful, please share it with your friends and family members. By spreading the word about how to read auto insurance policy, we can help more people protect themselves and their assets.